Fill Out Your Cg 20 10 07 04 Liability Endorsement Form

Cg 20 10 07 04 Liability Endorsement - Usage Guidelines

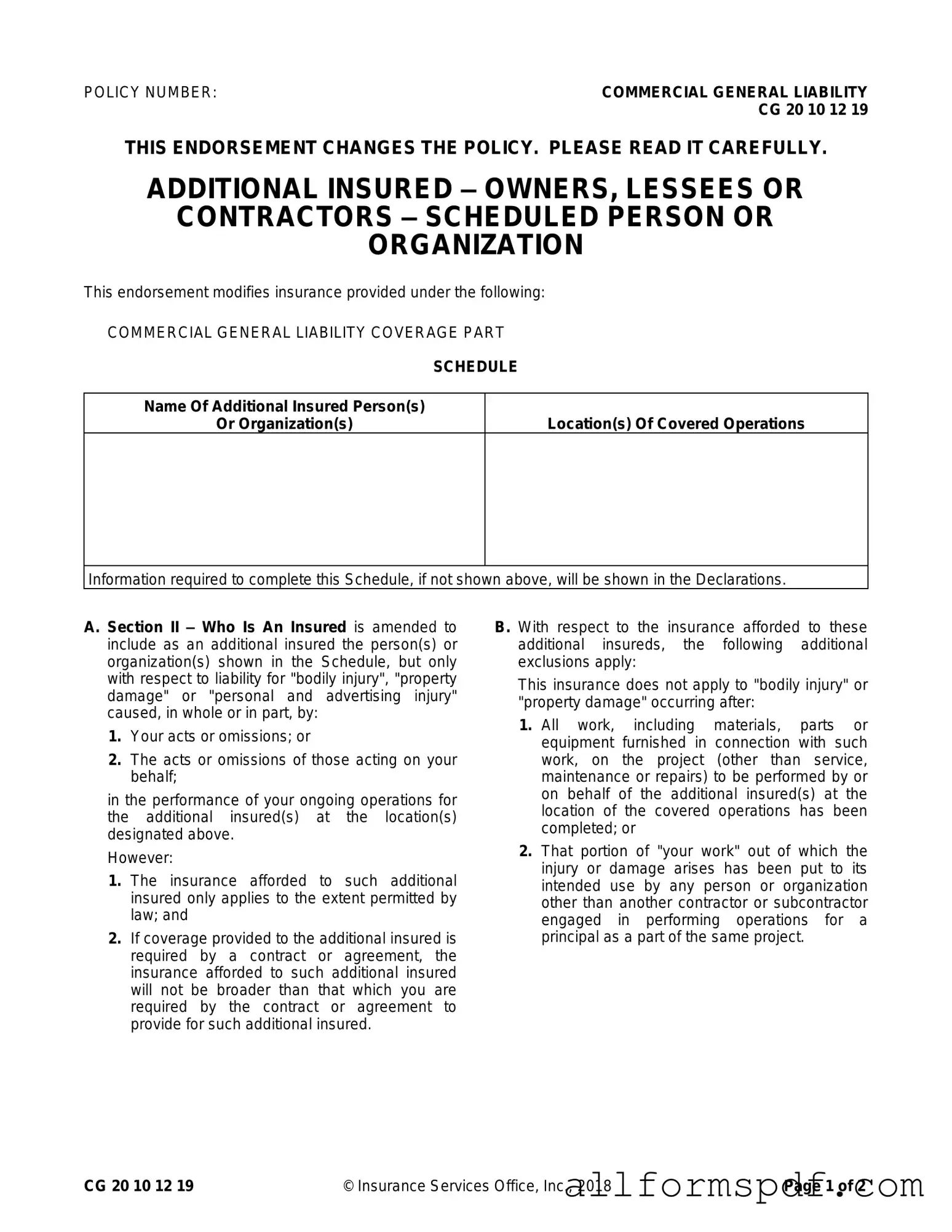

Completing the CG 20 10 07 04 Liability Endorsement form is a straightforward process. This form is used to add additional insured parties to a commercial general liability policy. Follow the steps below to ensure that all necessary information is provided accurately.

- Locate your Policy Number. This number is essential for identifying your insurance policy.

- Fill in the Name of Additional Insured Person(s) or Organization(s). Include the full legal names of all parties you wish to add.

- Specify the Location(s) of Covered Operations. Clearly state where the operations related to the additional insured will take place.

- Review the Schedule section. Ensure that all information is accurate and matches the declarations in your policy.

- Sign and date the form. This indicates that you agree to the terms and that the information provided is correct.

After completing the form, submit it to your insurance provider. They will process the endorsement and update your policy accordingly. Keep a copy of the completed form for your records.

Misconceptions

Misconceptions about the CG 20 10 07 04 Liability Endorsement form can lead to misunderstandings regarding coverage and responsibilities. Here are six common misconceptions explained:

- All parties are automatically covered. Many believe that simply listing an additional insured guarantees coverage for all claims. However, coverage only applies to specific liabilities related to the additional insured's operations.

- This endorsement provides unlimited coverage. Some assume that the endorsement increases the overall policy limits. In reality, the coverage for additional insureds cannot exceed the limits specified in the policy or required by contract.

- Coverage applies to all types of claims. A common misunderstanding is that the endorsement covers all claims made against the additional insured. In fact, it only applies to claims related to "bodily injury," "property damage," or "personal and advertising injury" arising from the named insured's operations.

- Coverage is effective regardless of contract terms. Some people think that the endorsement provides coverage without regard to any contractual obligations. However, if coverage is required by a contract, it will only be as broad as what the contract stipulates.

- Completed operations are always covered. There is a belief that all completed work is covered under this endorsement. This is incorrect, as coverage does not apply to injuries or damages occurring after all work has been completed or when the work has been put to its intended use.

- There are no exclusions for additional insureds. Many assume that additional insureds have the same coverage as the primary insured. In fact, there are specific exclusions that apply, which can limit the scope of coverage for the additional insured.

Understanding these misconceptions can help ensure that all parties are aware of their rights and responsibilities under the CG 20 10 07 04 Liability Endorsement form.

Dos and Don'ts

When filling out the CG 20 10 07 04 Liability Endorsement form, keep the following tips in mind:

- Do read the entire form carefully before starting.

- Do provide accurate information for the policy number and additional insured names.

- Do ensure that the locations of covered operations are clearly specified.

- Do double-check for any required signatures before submission.

- Do keep a copy of the completed form for your records.

- Don't leave any sections blank unless instructed to do so.

- Don't use abbreviations that may confuse the reader.

- Don't submit the form without verifying the information for accuracy.

- Don't forget to check if any additional documents are needed to accompany the form.

Other PDF Forms

Gf Applications - A puzzle solver who enjoys challenging games and brain teasers.

Hazmat Bol Template - It is essential to state whether charges are prepaid or to be collected upon delivery.

When engaging in the sale of a vehicle in Florida, it is important to fill out the necessary documentation to ensure a smooth transaction. The Florida Motor Vehicle Bill of Sale form acts as a crucial document that records the sale, detailing the agreement between buyer and seller. To assist in this process, you can find additional resources and templates at All Florida Forms, ensuring that all vital details such as make, model, year, and VIN are documented properly.

Voluntary Termination of Parental Rights South Carolina - Affidavit signatures must match identities as stated in the document.

Common mistakes

Filling out the CG 20 10 07 04 Liability Endorsement form can be straightforward, but several common mistakes can lead to issues down the line. One major error is leaving the policy number blank or incorrectly filled in. This number is crucial for identifying the specific coverage being modified. Without it, the endorsement may not be processed correctly, leaving the parties without the intended protection.

Another frequent mistake involves failing to accurately list the additional insured persons or organizations. It is essential to ensure that all names are spelled correctly and that the right entities are included. Omitting an additional insured can create gaps in coverage, potentially exposing parties to liability that the insurance was meant to cover.

People often overlook the importance of specifying the location(s) of covered operations. This section must be filled out precisely. If the locations are not clearly defined, it may lead to confusion about where the coverage applies, resulting in disputes if a claim arises.

In addition, some individuals neglect to review the contractual obligations related to the endorsement. The coverage provided cannot exceed what is required by the contract. If the form is filled out without considering these terms, it could lead to insufficient coverage, putting the insured at risk.

Lastly, it is common for applicants to misinterpret the exclusions outlined in the endorsement. Understanding when the insurance does not apply is crucial. Failing to grasp these exclusions can lead to unexpected liabilities after the fact, as coverage may not extend to certain situations that the insured believed were protected.

Key takeaways

When filling out and using the CG 20 10 07 04 Liability Endorsement form, consider the following key takeaways:

- Policy Number: Ensure the correct policy number is indicated at the top of the form to avoid processing errors.

- Coverage Modification: This endorsement modifies the existing Commercial General Liability Coverage. Review all changes carefully.

- Additional Insured: Clearly list the names of any additional insured persons or organizations in the designated section.

- Location Specificity: Specify the locations of covered operations accurately to ensure proper coverage.

- Liability Scope: The endorsement provides coverage for bodily injury, property damage, or personal and advertising injury caused by your actions or those acting on your behalf.

- Legal Limitations: Coverage for additional insureds is subject to legal limitations and cannot exceed what is required by contract.

- Exclusions: Understand that coverage does not apply if the injury or damage occurs after the completion of work at the designated location.

- Intended Use: If the work has been put to its intended use by others, coverage may be limited or excluded.

- Insurance Limits: The maximum payout for additional insureds will be the lesser of the contract requirement or the policy limits.

- No Increase in Limits: This endorsement does not increase the overall limits of insurance provided under the policy.